Should you pay down student loans early? Conventional wisdom says yes, and was reinforced at a SoFi event in San Francisco earlier this spring. They called up one of their members – she paid off her student loans early, and received a huge applause.

I was not one of the people clapping.

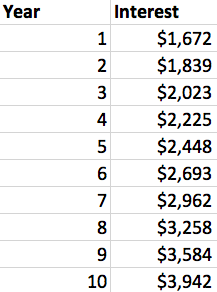

The member would have doubled her money’s return had she invested instead. When you compound the returns over years, she cost herself thousands in opportunity cost.

Student Loans Have Incredibly Low Rates

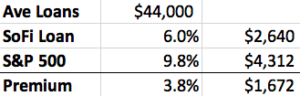

SoFi offers incredible interest rates, with student loans ranging from 3.9% – 8.18%. The rates are low, and the S&P 500’s average annual return over the past 90 years is 9.8% Assuming SoFi loan interest is right in the middle at 6%, you’re sacrificing 4% in annual returns by paying off your loans early instead of investing in an ETF.

This adds up – assuming she paid the average $44,000 grad school amount early, she would have made nearly four thousand dollars more if she invested that amount in the S&P 500 instead:

When Does It Make Sense to Pay Down Loans Early?

Your rule of thumb should always be to invest your money in the asset that gives the highest yield. Historically, this has been stocks, but there are times where it may make sense to pay off your debt early.

The monthly payments are so high you can’t save in your tax differed accounts

If your monthly payments are so high that you don’t have enough left over to invest in your 401k, or IRA, then I suggest paying down your principle to a point where you can afford to invest in your tax differed accounts.

Your tax differed accounts should be maxed out every year in your hierarchy of savings. Doing so will save you a killing in taxes.

You panic sell your investments if the market goes south

One thing is for sure about paying down your student loans – the interest you save is guaranteed.

The stock market is risky, and the economy is uncertain. Stocks go up in the long run, but can go down as much as 40% in a year.

There is no point in worrying about downturns, they can happen at any time. The real question is – how have you reacted to previous market downturns?

When stock prices go down, they’re on sale, meaning you should buy more. Unfortunately, too many people reach the other way. If you’re one of those individuals, I suggest paying down your debts first.

The market is overvalued

The best way to maximizing returns is to buy at a low price. The higher the market is, the lower your returns over time will be.

Many people claim that US stocks are already overvalued, and suggest paying down debts and diversifying risk. While many stocks are currently expensive, there are deals to be had in industries such as semiconductors, or regions such as China. Just because one asset class is overvalued, does not mean that there are no options to invest.

With that said, there could come a time where everything is overvalued. If that happens, I definitely suggest you pay down student loans early.

You want to buy a house

Lenders require your debt-to-income ratio to be under a certain limit, which is roughly 40%. If you’re a law school grad paying $2,000 in monthly payments while making a $72,000 salary ($6,000 per month), you’ll likely get turned down if the mortgage is over $400 per month.

With your extra money, you could either negotiate a refinancing of your student loans, or pay down the principle of your mortgage to meet the necessary debt to income threshold.

Your student loan interest is over 8%

The higher your student loan rates, the more sense it makes to pay them down instead of invest. Even a 1% higher return is meaningful as you compound that over years, but the higher the interest rate, the more risk you have investing instead of paying down your student loans early.

Pay Down Student Loans Early – The Bottom Line

One of the keys to wealth is using other people’s money, and low interest debt is an excellent way to compound your net worth. By investing that money and paying the minimum interest payments, you’re maximizing your returns, which will make a huge impact later in life.