You have done a great job saving – now comes the hard part, how to save your money effectively.

![]()

There are many vehicles to place your savings – including a standard brokerage account, 401k, IRA, or investing in assets such as real estate.

To help you prioritize your investments, we put together a hierarchy of where to save your money in order. Our mindset is to minimize your tax base, which is one of the largest wealth destroyers there are.

Check out the list below, and feel free to reach out or comment if you have questions or other thoughts

Maximize Your 401k

If you work for a company who offers 401k benefits, your first goal should be to max this out every year. Many companies match your 401k contributions up to a certain amount, meaning you are guaranteed to get a 100% return on that limit. When you think about how to save money effectively, you can’t beat a guaranteed 100% return.

For example, if your employer matches up to 5% of your 401k contribution, and your 5% contribution is $5,000. Your employer will provide an additional $5,000, giving you a total savings of $10,000!

Even if your employer doesn’t match, 401k contributions offer two other huge tax advantages. They lower your income taxes, and the money you invest will accrue tax-free until withdrawal.

How 401k Lowers Your Income Taxes

Let’s suppose you’re paying 40% in income federal and state income taxes. If you contribute $10,000, you just saved yourself $4,000 in income taxes ($10,000 x 40% = $4,000 savings). Had you decided to keep this money, you would’ve received only $6,000.

Such a tax savings is huge, and everyone can realize this savings, regardless of income.

While the 401k lowers your income taxes, most 401k plans charge unreasonably high rates. Therefore, if you change jobs or retire, we strongly encourage you to rollover your 401k into an IRA. You will save a ton in fees as each year goes by.

401k Lowers Your Capital Gains & Dividends Taxes

Once you contribute to your 401k, those savings will grow tax-free until withdrawal. Therefore, any sales or dividends you receive will not be subject to taxes.

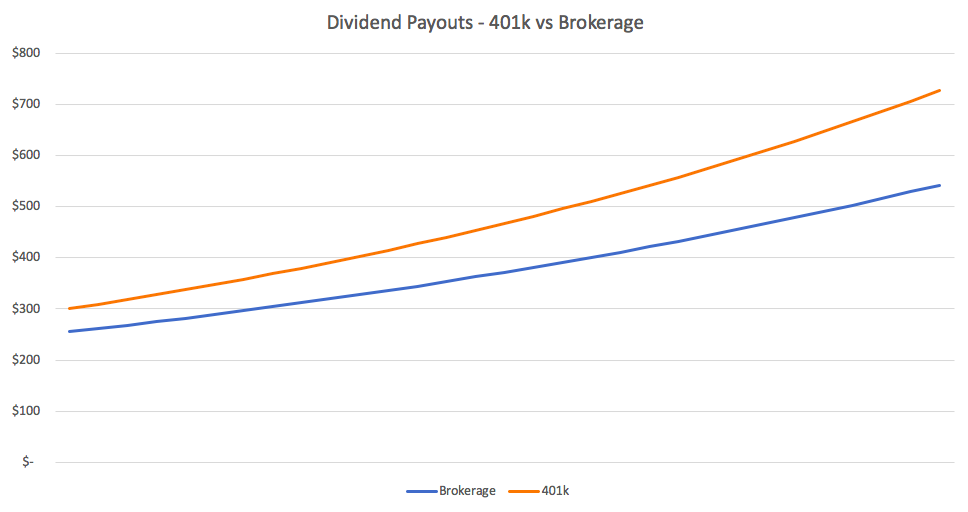

Using the $10,000 example again, if you invested this in the brokerage account and bought a stock paying a 3% dividend, you would earn $300 in dividend income per year.

Unfortunately, this money will be subject to capital gains taxes. At 15% capital gains, your take-home pay will actually be $255. When you factor in those capital gains over 30 years, your dividend check takes a serious hit.

Over 30 years, your dividend check is 34% higher thanks to the tax savings. Assuming that there is no stock appreciation, you save nearly $2,100 in capital gains taxes.

Maximize Your IRA

Once your 401k is maxed out, your IRA is next. You can contribute up to $5,500 in your IRA per year, and you can fully deduct this from your income taxes if your income was less than $118,000.

If you made more than $133,000 in 2018 – congratulations, you’re in the top 92.2% of earners in the United States. Unfortunately, you will not be able to deduct any of your IRA contributions in your taxes.

Even if you cannot deduct this, you will still save capital gains as your investments grow and dividends are paid back into the account. As we calculated previously, that savings will add up over time.

What About a Roth?

If you make less than $120,000 in 2018, you could contribute to a Roth IRA instead of an IRA as well. With a Roth, you pay taxes up front instead of deducting them, and your withdrawals will be tax-free.

While people who earn over $120,000 cannot directly contribute to a Roth, any IRA holder can convert some of their IRA to a Roth as well. The key consideration is whether you’ll be in a higher income tax bracket now, or at retirement. Since most of us will be earning less money during retirement, we’ll likely be at a lower bracket in the future.

Buy a Home

Once you maxed out your 401k and IRA, the next big tax saver to consider is your home. Taxpayers can deduct interest paid on their first and second home mortgages that have up to $750,000 in mortgage debt. For everyone outside of San Francisco and New York, that’s more than enough.

If you have a $500,000 mortgage paying 4.5% interest, you’ll have roughly $22,500 that can be deducted each year. This goes down as you pay more of your principle, but you can always refinance this in the future.

At the 24% tax bracket, which is making over $82,500, you’ll save $5,400 on interest alone. When you think about how to save money effectively, this tax savings will really add up.

While this is a great way to save in taxes, we recommend spending no more than 30% of your take home pay on housing. Any higher percentage will compromise your ability to max out your 401k and IRA, and homes are not a great investment.

Furthermore, spending too much on housing could make you house poor, which is a terrible situation to be in.

Remember, you can deduct these interest expenses on two properties. A rental property near your home could be a great way to generate income while lowering your tax burden.

Max Out Your Health Savings Account

Health Savings Accounts, or HSAs, are a great way to pay for your future healthcare. Each individual can contribute up to $3,450 per year, which can add up to a great nest egg at your retirement.

The Rest Goes in Your Brokerage

After maxing out all of your tax savings, the rest of your money should go in your general brokerage account. We recommend ETFs that track the S&P 500, as does Warren Buffett, and strongly advise staying away from mutual funds. Mutual funds are a ripoff, so stay away from them.

How to Save Money Effectively – The Bottom Line

While saving your money is important, it is just as crucial to know how to save money effectively. By prioritizing your savings with the right vehicles, you’ll lower your tax burden and grow your net worth at a much higher velocity.

We recommend maxing out your 401k first, and then your IRA. After that, owning a home can make a serious dent in your taxes. Finally, maxing out your HSA will leave you with a nice nest egg for your future healthcare costs.

Now that you know how to save money effectively, the trick is to do it. While this will take time, you’ll be set up for a great retirement and future by following this path.