The average mutual fund fees had an expense ratio of 1.25% in 2017. ETFs, on the other hand, charge a .08% expense ratio. Therefore, the average mutual fund fees charge a 1,562% premium to Vanguard ETFs.

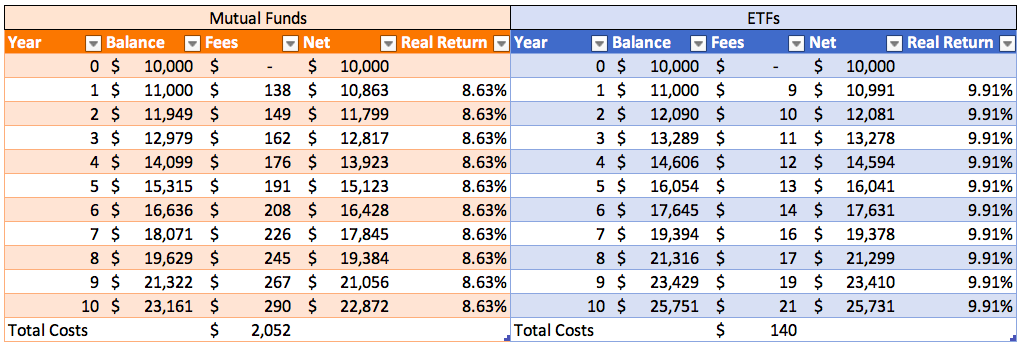

These expenses really add up, which is why we strongly encourage you to avoid them. Here is a side by side comparison of mutual fund and ETF fees once you factor in their costs. Even with $10,000 in the bank, the expenses will make a serious blow to your future net worth.

For this example, we are going to assume that you have $10,000, and that both funds are performing as well as the S&P 500, earning a 10% average return per year. This may be a generous return for mutual funds, as we’ll explain later.

The difference is staggering, and is why we feel so strongly about avoiding mutual fund fees. Over the course of 10 years, you paid over $1,912 more for your mutual fund account. Even worse, your expenses were no longer compounding, meaning that your mutual fund has $2,590 less than your ETF account. That $2,590 difference is over 11% of your mutual fund portfolio.

This is why we have such a strong position on mutual fund fees. While that 1% or 2% may seem like peanuts, the expense becomes a huge number over time. Since you can contribute up to $18,500 in your 401k each year, the costs can grow to astronomical levels.

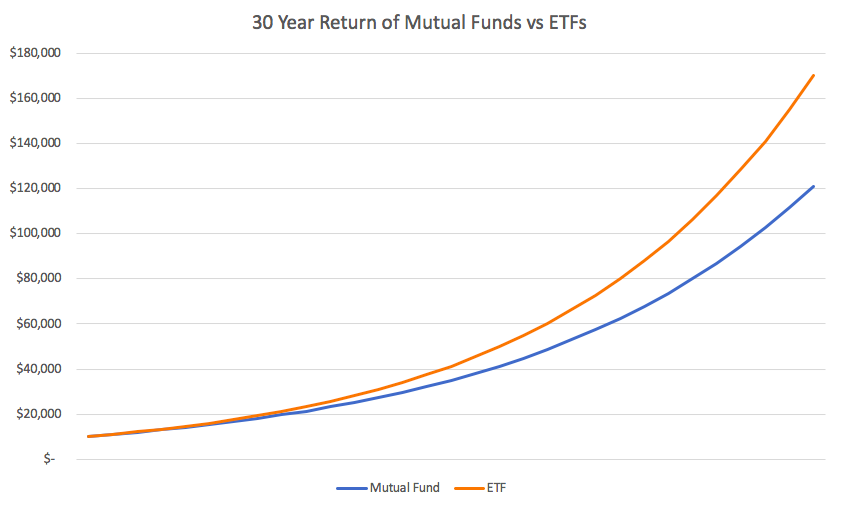

Just take a look at how large this difference becomes after 30 years. Over 30 years, you’ll have $170k if you invested in ETFs, whereas just $120k with mutual funds.

Mutual Fund Performance

You get what you pay for at least, right? By paying such a premium, the mutual funds better beat the market! As long as they beat the market by their expense ratios, you’re better off investing in them.

Various studies show that very few mutual funds beat the market. In fact, 95% of finance professionals do not beat the market over 10 years. Meaning you have a 5% shot of finding one that will.

So if you aren’t getting a higher return, what else are you getting? Possibly more stability, but is it worth the price you’re paying? Would you rather have more money or less volatile returns?

What Fees Mutual Funds Charge

Mutual funds have a lot of fees baked into their portfolio. Expense ratios are the most commonly viewed, and there are a few others to consider as well.

Expense Ratios

As we described earlier, these are the most common fees associated with mutual funds. It is normally expressed as a percentage – these fees cover the costs of the fund’s employees and operating costs.

12B-1 Fees

The 12B-1 fee is an annual marketing and distribution fee for a mutual fund. This sometimes gets sold as a benefit to investors. By marketing the fund and acquiring more investors, the theory goes that your expense ratios will be lowered thanks to economies of scale. While the theory makes sense, we have never seen it happen in practice. Mutual funds should acquire investors thanks to performance and low costs, which is why we recommend keeping your money in ETFs instead.

Sales Commissions

If you have a broker invest on your behalf, they will likely charge a fee for their service as well. Brokers could have a conflict of interest to sell funds that pay them more, instead of funds that are in your best interest. We have our feelings about working with brokers and financial advisors – if you decide to work with one, beware of this conflict.

Trading Commissions

Whenever the mutual fund makes trades, costs are incurred and are charged separately. These charges are nominal in the grand scheme of things.

Mutual Fund Alternatives

Exchange traded funds (ETFs) are an incredible alternative to mutual fund fees. With an average expense ratio of .08%, Vanguard’s ETFs charge a fraction of the cheapest mutual funds. Fidelity even offers ETFs that are completely free. Paying a lower fee will increase your overall return, which becomes a huge number as it compounds over time.

Another alternative is to invest in your own stocks. While this option is out there, it’s not for the faint of heart. If 95% of finance professionals cannot beat the market over 10+ years, what are the odds that you’ll do better?

Investing in your own stocks is a terrific hobby, and a great skill to learn that you can improve throughout your life. With that said, we don’t recommend allocating a large portion of your net worth to individual stocks until you have spent a lot of time reading and learning. Once you have, we recommend you spend at least 10 hours per week managing your investments.

Mutual Fund Fees – The Bottom Line

Mutual fund fees cost a ton of money, and 95% of them actually do worse than the overall market. Trillions of dollars are sitting in mutual funds, making them a giant tapeworm on our economy.

To maximize your savings, we recommend setting your money in ETFs instead. There are tons of ETFs that track different industries, countries, and commodities. Although there are so many options, we recommend keeping it simple with the S&P 500. Even Warren Buffett believes that low-cost S&P 500 index funds are the best for retirement.

While individually owning stocks is a fun hobby, we don’t recommend making this a large portion of your portfolio unless you’re willing to put in 10+ hours per week managing your investments.

By allocating the majority of your net worth to low cost index funds, your savings and net worth will be dramatically higher when the time comes from retirement. We live in an incredible time where investing couldn’t be more affordable, make sure you take advantage of it!