Personal savings account rates have been trending up in 2018, with rates getting as high as 2.05%.

While that is certainly the highest return we have seen in 5 years, it also doesn’t factor inflation. The United States Federal Reserve targets 2% for inflation, meaning that it will eat away nearly 98% of the returns in your personal savings account. Once you include inflation, you’re only netting a .05% return on a 2.05% savings account.

We recommend keeping at most 6 months of living expenses in your savings account. Doing so will ensure you don’t have to sell any long-term investments at the wrong time for a rainy day. That amount is also low enough where you won’t experience a huge drag on your returns by keeping cash on the sidelines.

Below we will dive deeper on inflation, how it eats away into your savings, and the profound difference inflation when you compare personal savings accounts and the stock market over 10 years.

What is Inflation

Inflation is the rising price of goods and services over time. It means that over time, a dollar will not buy as much as it will today.

We hear about this when our grandparents talk about how they could buy a Coke for a nickel. It’s not that soda was dirt cheap back then, the dollar just had a lot more purchasing power.

Central banks will manage inflation, and the United States Federal Reserve actually has a 2% target for annual inflation. Through monetary policy, they will balance inflation with unemployment, and ensure that inflation does not get out of hand.

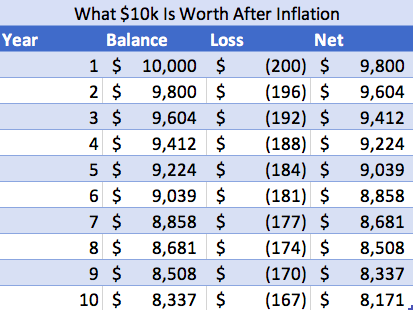

Since the United States targets 2% for annual inflation, you need to factor that into your personal savings returns and retirement. That 2% is just small enough for us to notice it, but it really adds up over 10 years. Even at 2%, $10k today will be worth roughly $8k in 10 Years

Why Inflation Eats Away Your Savings Account

The highest personal savings accounts in October 2018 are 2.05%. Since we know the US Federal Reserve targets 2% inflation, that means you should only expect to make .05% on your personal savings account. This means that inflation will eat away 97.6% of the gains from your savings account.

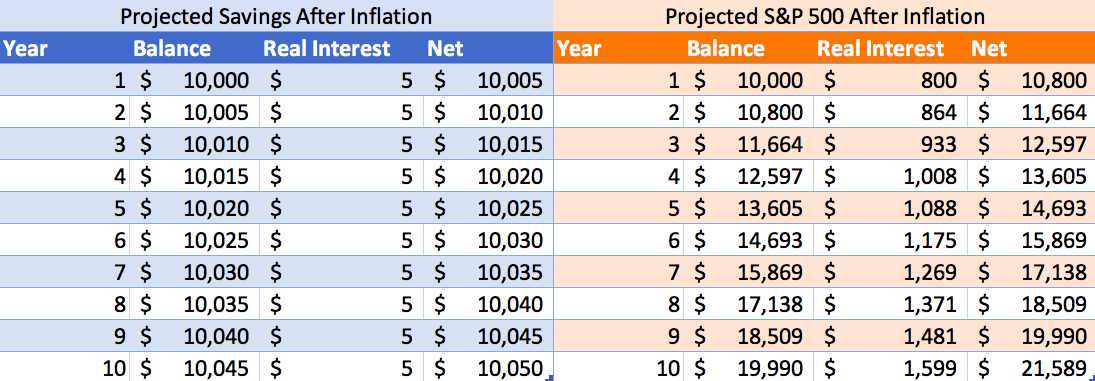

Obviously inflation should be factored into the stock market as well, which historically returns 10% per year. With that said, the federal reserves 2% inflation target will only eat away 20% of your stock market returns. This means that inflation has 4.9x more of an an impact on personal savings accounts than stock investments.

That difference is profound even after 10 years. $10k in a personal savings account will be worth $10,050 in today’s money. In stocks, that same $10k will be worth nearly $22k in today’s dollars.

How Much Should You Have in Savings?

We recommend having at most 6 months of living expenses in your savings account. Therefore, if you spend $2,000 every month, we recommend having $12,000 in your savings account. Everything else should be devoted to long-term investments such as stock investments or real estate. We define long term as 5+ years.

Any extra money in savings may feel rewarding since you have a bigger cushion. In reality, you’re increasing your opportunity costs for alternative investments. Any additional money could be earning your more income, so you should treat that loss in potential earnings as an expense.

Inflation & Your Personal Savings – The Bottom Line

Inflation is a cost that few people factor into their investing. Once you do, you realize that your savings account is not making you as much as it seems. In fact, it could easily be losing you money.

Only keep the minimum cash you need in personal savings, which we recommend to be 6 months of living expenses. This will ensure that you don’t have to sell any of your long term investments if something happens. Any more money than 6 months of living expenses is unnecessary, and prevents you from maximizing your returns from more lucrative investments such as stocks or real estate.

Inflation is a necessary evil of growth. Our central banks will do their best to manage it, and you should keep that in mind for all of your investments. Once you do, you’ll realize that savings accounts will not return anything near what you think.