The 50/30/20 Rule is a great format for anybody new to budgeting. Determining how much to spend on housing, social events, dating, and everything else in life can be daunting. If you don’t lay the right budget foundation, your savings could easily fall by the wayside.

![]()

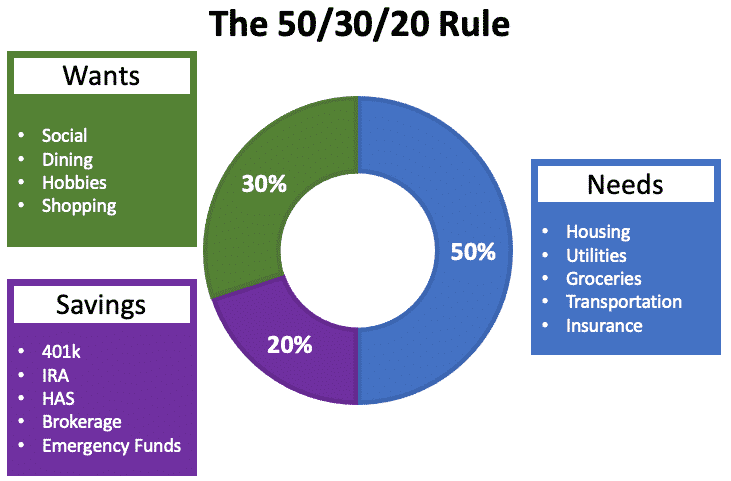

There is a huge opportunity cost when you don’t save early. With the 50/30/20 rule, you split your after-tax income into 3 buckets between savings, needs, and wants. This ensures you’re putting enough in savings, which will set you up for a wealthier financial future.

Calculate Your After-Tax Income

Taxes are a sure thing in life, so you’ll want to subtract them before you start budgeting. You can determine your after-tax income by subtracting your taxes, medicare, and social security. This is easy to determine if you’re an employee, simply look at your paycheck and deduct the appropriate expenses.

If you run your own business, you’ll be responsible for calculating and paying your quarterly taxes.

20% of Your Income – Savings

Many recommend budgeting for needs, then wants, and the rest for savings. We believe this is a mistake. Pay yourself first in savings, then use the rest to accommodate for needs and wants. Compound interest is an incredible force, and you’ll realize those benefits the sooner you start saving and investing.

Repaying debt is also part of savings. The importance of debt repayments depends on the interest level. If you have credit card debt charging 25% interest, definitely pay that down before you invest a nickel into anything else.

If you have low interest student loans, however, it likely makes sense to pay the minimum and invest the rest instead. Student loans have very low rates, so we don’t recommend paying them down early.

50% of Your Income – Needs

Needs are the essentials such as housing, groceries, utilities, transportation, and insurance. Anything that would severely impact your life or career is considered a need.

It is important to classify needs versus wants. For example, taking the bus to work would be considered a transportation need. Taking Uber instead would be a want, since it is a more convenient way to get to work. If a car is a need for work and travel, make sure you follow the 1/10th rule when you buy a car.

Do not treat your housing as savings. Too many people put all of their net worth into their house, which is not liquid and has too many transaction costs. If you spend too much of your budget on housing, you could end up house poor, where all of your income is needed to cover your house.

30% of Your Income – Wants

Wants are everything outside of your needs. Dining out, social events, and hobbies would all be considered a want.

It’s easy to justify wants as a need. You “need” designer shoes to look professional at work, or you “need” to go to a networking event to advance your career.

To sanity check needs and wants, ask yourself “will my life or career be severely limited without this?” Let’s test this on our two examples:

- As long as you have professional shoes, nobody is going to fire you

- If you miss a networking event, your career will be just fine

Under this sanity check, you can see that both examples are wants, not needs. This applies to the 1/10th rule of buying a car as well. A 2000 Honda Civic will get you to work just as easily as a 2018 BMW. The Civic would be a need, and spending more for a nicer car is a want.

There are many ways to keep your costs down. The less you spend on needs and wants, the more money you can put into your savings.

The 50/30/20 Rule – The Bottom Line

The 50/30/20 rule is a great format to start budgeting. The numbers are simple, and it puts a lot of money in savings.

Unlike most, we recommend starting with savings. Invest in yourself before you decide how much to spend on housing and wants. It’s easy to stretch these initial expenses, which could force you to sacrifice the amount you dedicate to savings.

While 20% is a great start for savings, you should increase this percentage as your salary increases. Too many people deal with lifestyle inflation, where they continue spending more on needs and wants as they make more money.

Pay yourself first instead. The more you save now, the more flexible you’ll be in the future. If you instead spend more on wants and needs, you’ll be in a tough spot if you want to take a less stressful job that pays less. You also won’t be able to retire as early.

The 50/30/20 rule is a great start to ensuring this financial flexibility, just remember that 20% should never be your ceiling for savings.