Financial Independence Retire Early, known as “FIRE”, has grown from a group of bloggers to being featured in the Wall Street Journal and New York Times. More and more people are striving towards financial and personal freedom, and the FIRE movement aligns with this.

We’ll walk through what FIRE is, how to do it, and what risks you should keep in mind.

What Is FIRE?

FIRE stands for financial independence, retire early. The goal of FIRE is to maximize savings by cutting expenses so you can become financial independent and retire when you’re ready.

The movement has spread to two different branches. One group is called the “lean” FIRE movement, and the other is the “fat” FIRE movement.

The leanFIRE group lives in in extreme frugality, who focus more on maximizing savings than by earning more. They are minimalists who follow strict budgeting goals. Reddit has a leanFIRE group with over 61k subscribers, and say the group is for anyone who wants to retire before 60 with less than $40k in planned yearly expenses. Since the average income for Americans is roughly $46k per year, this group will apply to most Americans.

The fatFire movement is less strict towards budget, and focuses more on maximizing earnings and investing wisely. Since most people do not make high enough salaries for fatFIRE, they don’t have as big of a following. In fact, Reddit’s fatFIRE group has 1/3 as many subscribers compared to the leanFIRE group.

How to FIRE

The FIRE movement lives by three key themes, and they all revolve around having more money to save.

Make sure you invest the extra money based on your hierarchy of savings. Although tax-deferred assets cannot be accessed until you’re older, it’s a mistake to walk away from the immediate income tax savings and capital gains savings. Maximize those first, and then place the rest in stocks such as an S&P 500 ETF. Warren Buffett claims that this is the best investment for most people.

Frugality

FIRE stresses saving your money and budgeting aggressively. Their logic is that the more you save now, the sooner you can retire later.

Frugality can go overboard, though. If you go this route, make sure you’re being frugal without looking cheap.

Minimalism

People pursuing FIRE believe in doing more with less. Don’t spend too much on a car, and don’t own too big of a house.

There’s another benefit to minimalism. By owning less stuff, you have less stuff to worry about. Minimalism has many psychological benefits outside of money.

Extra Income

The more money you make, the more you’ll be able to save. In my opinion, the FIRE movement does not talk enough about this. People assume that they’re stuck at whatever salary they have.

I completely disagree, you can always invest in yourself and negotiate for raises. You can also invest your time in side hustles or start a business. In addition to the extra paycheck, you’ll learn more marketable skills. This is an often overlooked part of the FIRE movement.

As you make more money, just make sure you don’t succumb to lifestyle inflation. Save the extra money you’re making.

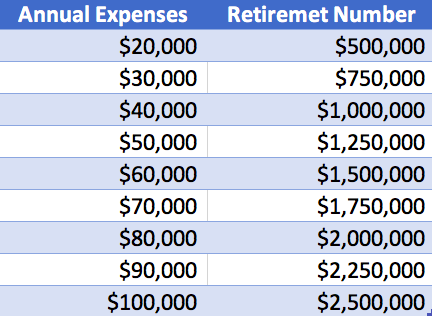

How to Calculate Your FIRE Date

The FIRE communities all have a target number that they’re working towards. This is typically calculated using the 4% rule. The logic is that you can safely withdraw 4% of your investments every year without compromising the principle amount.

Divide your annual expenses by 4% to determine your ideal number. For example, if you spend $30k per year in expenses, you would want $750k in investments and real estate.

Here’s a table showing what your retirement number needs to be based on a range of expenses.

The Risk of FIRE

FIRE has one major risk. If you run out of investment income, you will have to enter the workforce. After being out of the game for so long, odds are that you will have a very tough time finding a job that pays anywhere near what you made before.

Make sure you keep these items in mind as you’re looking to FIRE.

Over-Estimating Investment Performance

The market has been on a bull run for the last 9 years, but that won’t happen forever. Don’t assume that past returns will lead to future performance.

Instead, keep in mind what your asset class returns on average, and understand the premium you’re paying for the asset. The more you’re paying for a piece of real estate, or for a slice of the S&P 500, the less you’ll return in the future.

Lowballing Living Expenses

Your medical expenses will be a lot higher when you’re 60 compared to when you’re 20, and not enough people keep that in mind.

Unexpected costs could go up in a multitude of ways. From higher health care costs, to higher property costs, to higher taxes. Make sure your expenses model has a high degree of sensitivity before you leave the workforce.

Becoming Too Dependent on Government Programs

Many leanFIRE groups recommend a budget that allows you to capitalize on government programs once you leave your job. Quick question, what happens if those handouts disappear?

Several companies go out of business because they assumed that government benefits would last forever, make sure you don’t follow their mindset.

Financial Independence Retire Early – The Bottom Line

The FIRE movement has grown from a group of bloggers to being featured in the Wall Street Journal and New York Times. More and more people are striving for financial and personal freedom, and the FIRE movement aligns with this.

While there are multiple branches, the key tenant of FIRE is to maximize your savings. By earning more and spending less, you’ll be able to invest more money and reap the rewards of compound interest.

Make sure you take into account future expenses, such as health care or higher taxes. By accounting for those expenses, you’ll be able to spend your early retirement with a lot less stress.

With all of that said, I want to come out and say that I do not agree with retiring early. It never hurts to have some type of work going on in your life. Doing so ensures you stay “in the game” in case you do need to come back to work, and you continue having income.

Finally, work has more benefits than just money. There’s a social element to work that you would miss, so make sure you fill it with something.

Instead of “Financial Independence Retire Early”, I propose “Financial Independence Flexible Opportunities”. Let’s call it FIFO, and see how it takes off.