Shielding your income from taxes is a top priority as you make more money. Taxes are one of the largest wealth destroyers you’ll face, and a mega backdoor Roth will help you shield more money tax-free.

Mega backdoor Roths allow you to save as much as $37k every year tax-free, so you can imagine how much this adds up over several years.

Below is a breakdown of the different terms in 401k contributions, and how to maximize each of these in your hierarchy of savings.

What is a Mega Backdoor Roth?

Before explaining a mega backdoor Roth, there are 3 types of 401k contributions to understand: pre-tax, Roth, and after-tax.

Pre-Tax Contributions

Standard 401k plans are pre-tax contributions. Your contributions pay no income taxes, and the money grows until you withdraw the money. Pre-tax contributions should be maxed out first in your hierarchy of savings since it reduces your income taxes.

You will need to pay income taxes on the money you withdraw, but the tax savings from compounding your money means that you’ll have a lot more left over.

The 2019 limit for pre-tax contributions is $19,000.

Roth Contributions

If you contribute to a Roth 401k instead, they are considered Roth contributions, and the money is funded after you pay income taxes.

Since the money is made with after-tax money, the contributions will grow tax free, and can be withdrawn tax free once you retire.

We could write an entire article on whether you should contribute your 401k pre-tax or post-tax through a Roth 401k. My tax guy recommends funding pre-tax, and I echo his sentiment.

Odds are you are making more money now than when you retire, which means you’re at a higher income tax bracket today. Saving money pre-tax will be more meaningful. Finally, the government could always change this policy, and burn you if you contribute post-tax funds.

After-Tax Contributions

Finally, some plans allow you to make after-tax contributions in addition to your 401k. This is the key to a mega backdoor Roth.

After-tax contributions are made with money you have already paid tax on. The money grows tax free, and will be taxed again at the time of withdrawal.

Your maximum retirement contribution in 2019 is $56,000. To figure out how much you can contribute after-tax, subtract this $56k by the $19k you contribute in your 401k or Roth 401k, as well as your employer contribution.

For example, let’s suppose your employer contributes $5k. You would then subtract $56k by $19k + $5k, which means you can contribute an additional $32k after tax.

$56k Limit – $19k 401k / Roth 401k – $5k Employer Contribution = $32k

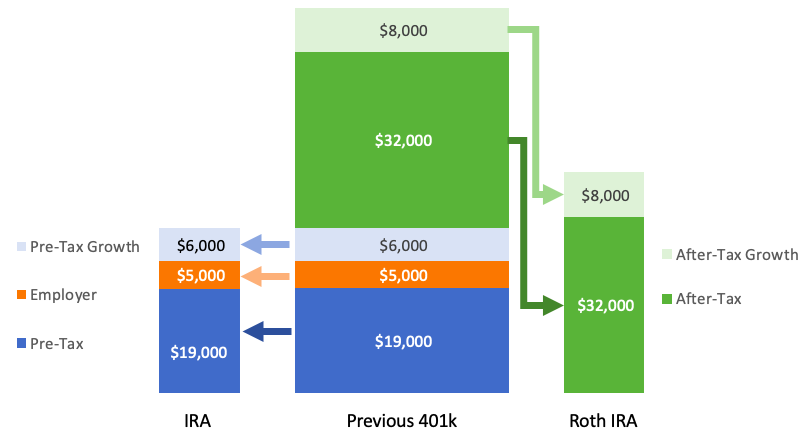

Moving Money from Your 401k to Your IRA

The IRS states that when transferring money from your 401k to your IRAs, you can rollover pre-tax portion of your 401k, as well as all of it’s investment growth, to a traditional IRA tax free.

Any of your after-tax contributions will rollover to a Roth IRA, which is huge for anybody who makes too much to contribute to a Roth IRA.

Example of Transferring Money

Let’s suppose you received a monster bonus on January 1st, 2019. With that bonus, you maxed out your $56k contribution. Here’s how that breaks down:

- Pre-Tax: $19k

- Employer Contribution: $5k

- After-Tax: $32k

We’ll fast forward an entire year. You interviewed at a couple companies during the year, and negotiated a huge pay increase.

While you negotiated a pay raise, your 401k also went up by 25%, and that $56,000 is now worth $70,000!

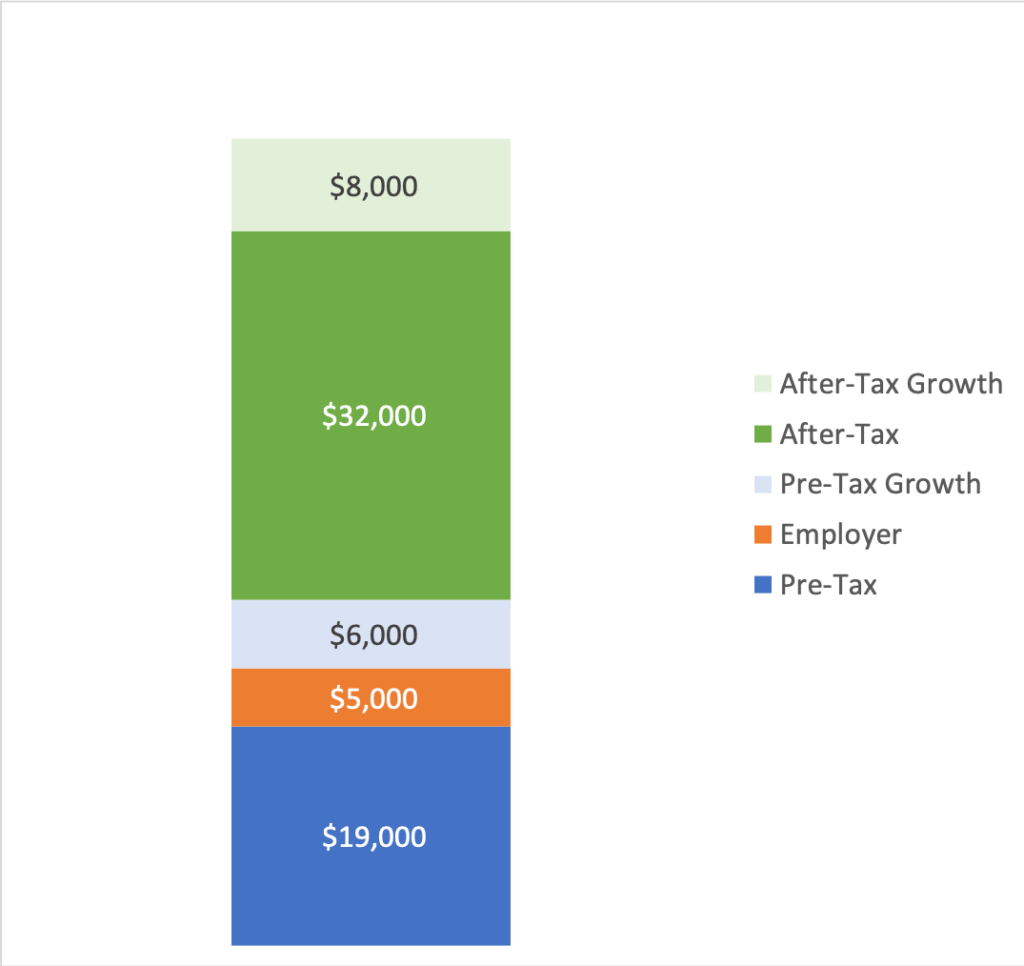

Here is what your new balance looks like:

You start your new job on January 1st, 2020, and rollover all of that money to an IRA. Since your pre-tax contributions and growth will be taxed, only your after-tax contributions will not be subject to tax once you withdraw the money.

- Blue: Not taxed at withdrawal

- Orange: Taxed at withdrawal

By waiting a year to roll your money over, only your original after-tax contributions will grow tax free. Once the money rolls over, that base will be able to grow tax free.

The Better Way – A Mega Backdoor Conversion

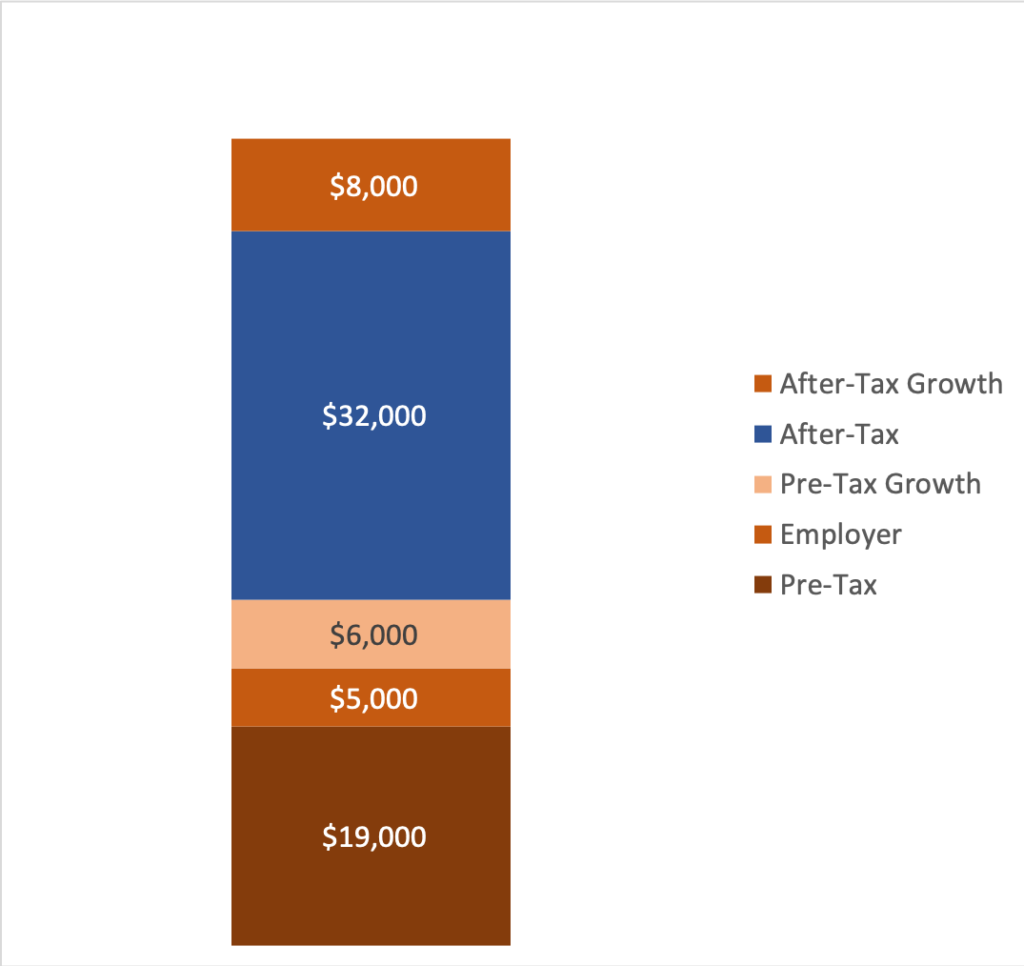

Suppose that instead of rolling over your 401k over a year from now, what if you immediately rolled the money over on January 1st, 2019?

According to the IRS, pre-tax contributions will go to a traditional IRA, and after-tax contributions will go directly to a Roth IRA.

Here’s what your IRA accounts will look like assuming you roll your 401k over immediately and realize 30% growth:

As you can see, your $8k in gains will sit in your Roth IRA, and will not be taxed. This money will grow exponentially over time, saving you a ton in taxes and maximizing your retirement savings.

Mega Backdoor Roth – The Bottom Line

The first two steps of the hierarchy of savings are to max out your pre-tax 401k, and then your IRA. Once these are maxed out, many employer plans will allow you to contribute more money after tax.

These contributions could be as high as $37k depending on how much your employer contributes. The sooner you can convert this money to a Roth IRA, the more money you’ll be able to shield from taxes.

If your employer does not allow after tax contributions, make sure to bug human resources until they make the change. Educate your colleagues on how much they can save in taxes with this strategy. If enough employees go to HR, the more likely you’ll get this added.

The same thing happened with my employer. After two years of bugging human resources, our company finally offered after-tax contributions in 2019. Be stubborn about adding this, your tax savings are more than worth it.

Finally, keep in mind that you are blessed to be in this position. If you are saving $56k per year, you’re saving more money than 67% of Americans earn every year. You’re in an incredible position, be grateful, don’t brag about it, and make the most of this opportunity.